If you’ve ever sat across from an investor and watched their eyes go straight to one line in your financial model, there’s a good chance that line was EBITDA. Founders often obsess over revenue growth and burn rate, but why EBITDA is important for startup valuation comes down to one simple truth: it’s the cleanest way to show how your business actually performs, stripped of the noise that makes comparisons messy.

So, what is EBITDA? It stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It’s a profitability metric that tells investors how much cash your core operations generate before it distribute to lenders, shareholders, & tax. This number can make or break a startup’s fundraising success.

In this guide, we’ll break down what EBITDA really means for a startup, why VCs and acquirers lean on it so heavily, what a healthy EBITDA ratio looks like, and the practical levers you can pull to improve it before your next raise.

What Is EBITDA

EBITDA measures the profit your business generates from running its actual operations, before you pay any interest, tax & deduct depreciation & Amortization.

There are two common ways to calculate it:

- From Net Income: EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization

- From Operating Income (EBIT): EBITDA = Operating Income + Depreciation + Amortization

The second formula is usually faster, since EBIT already excludes interest and tax. You’re simply adding back the two non-cash expenses: depreciation (wear and tear on physical assets like equipment) and amortization (the write-down of intangible assets like patents or software).

Here’s why that matters for a startup specifically. Imagine two companies with identical operations, but one carries a lot of debt and the other doesn’t. Net income would make the indebted company look weaker, even though its core business is performing just as well. EBITDA strips that distortion out, which is exactly why analysts and private equity professionals tend to favor EBITDA-based multiples over earnings-based ones when comparing companies.

Why EBITDA Is Important for Startup Fundraising

Most early-stage startups don’t have positive net income. Because of high upfront spend on product development, hiring, and customer acquisition, a young company can easily show a loss on paper while still building something genuinely valuable. This is exactly where the importance of EBITDA for startup valuation becomes clear: it lets investors look past temporary losses and judge the underlying health of the operating model.

A few reasons EBITDA carries so much weight in a raise:

It normalizes comparisons:

Two startups in the same industry can have wildly different debt loads, tax jurisdictions, or depreciation schedules. EBITDA puts them on equal footing.

It signals operational discipline:

A founder who can show a clear, improving EBITDA trend is telling investors, “I understand my unit economics and I can run this business efficiently, not just grow it.”

It supports valuation multiples:

In capital-intensive sectors, and increasingly in growth-stage tech and services businesses, buyers and investors price the company as a multiple of EBITDA rather than revenue, especially as the company matures past the early hyper-growth phase.

It’s a proxy for cash flow:

While not identical to cash flow, EBITDA gives a quick read on how much cash the business is generating before non-operating items, which matters a lot when investors are sizing up runway and debt repayment capacity.

It’s worth noting that a negative EBITDA isn’t automatically a red flag for an early-stage startup. Plenty of high-growth companies intentionally run negative EBITDA while they invest in customer acquisition and product development. What investors actually want to see is a believable, well-modeled path toward positive EBITDA, not necessarily positive EBITDA today.

Net Profit Can Lie. EBITDA Tells You What’s Really Happening Operationally

Here’s a comparison that comes up constantly in due diligence, and it confuses a lot of founders: two companies can have the exact opposite net profit and EBITDA story, and the one that “looks” worse on the bottom line can actually be the stronger business.

| Startup A | Startup B | |

|---|---|---|

|

Content |

$5M |

$5M |

|

Net Profit |

-$200K (loss) |

$400K (profit) |

|

EBITDA |

$900k (positive, healthy) |

$150K (weak) |

|

Why The gap? |

Heavy depreciation on new equipment + interest on a growth loan are dragging net profit down, even though operations are efficient |

Low debt and low depreciation keep net profit looking fine, but the core operations barely break even |

|

What An Investor Concludes |

Operating performance is strong. The loss is a financing and accounting story, not a business-model problem |

The business model itself isn’t generating much operating efficiency, profit is coming from accounting timing, not real operational strength |

This is exactly why investors don’t stop at net profit. Company A‘s net loss looks alarming on the surface, but once you isolate operations from financing (debt) and non-cash charges (depreciation/amortization), the EBITDA shows a business that’s fundamentally healthy and just structured aggressively around growth capital. Company B‘s net profit looks reassuring, but the thin EBITDA margin reveals the operations themselves aren’t producing much real efficiency, the profit is more fragile than it appears.

This is also where revenue growth alone can mislead founders. A startup can show impressive top-line revenue growth while EBITDA stays deeply negative, and at the pre-seed or early growth stage, that’s often completely fine, investors expect you to spend on marketing and customer acquisition to prove demand. But as the company moves toward scaling, that tolerance shrinks fast. Revenue growing 80% with a flat or worsening EBITDA margin starts raising a different question for investors: is this growth actually buildable into a profitable business, or is it growth that only exists because of unsustainable spending? Strong revenue without an improving EBITDA trend is one of the most common reasons later-stage rounds stall or get re-priced downward.

It’s worth noting that a negative EBITDA isn’t automatically a red flag for an early-stage startup. Plenty of high-growth companies intentionally run negative EBITDA while they invest in customer acquisition and product development. What investors actually want to see is a believable, well-modeled path toward positive EBITDA, not necessarily positive EBITDA today.

How EBITDA Impacts VC Decision-Making

Venture capitalists evaluate dozens of metrics, but EBITDA (and its trajectory over time) plays a specific role in how they think about risk and return.

It shapes the valuation conversation:

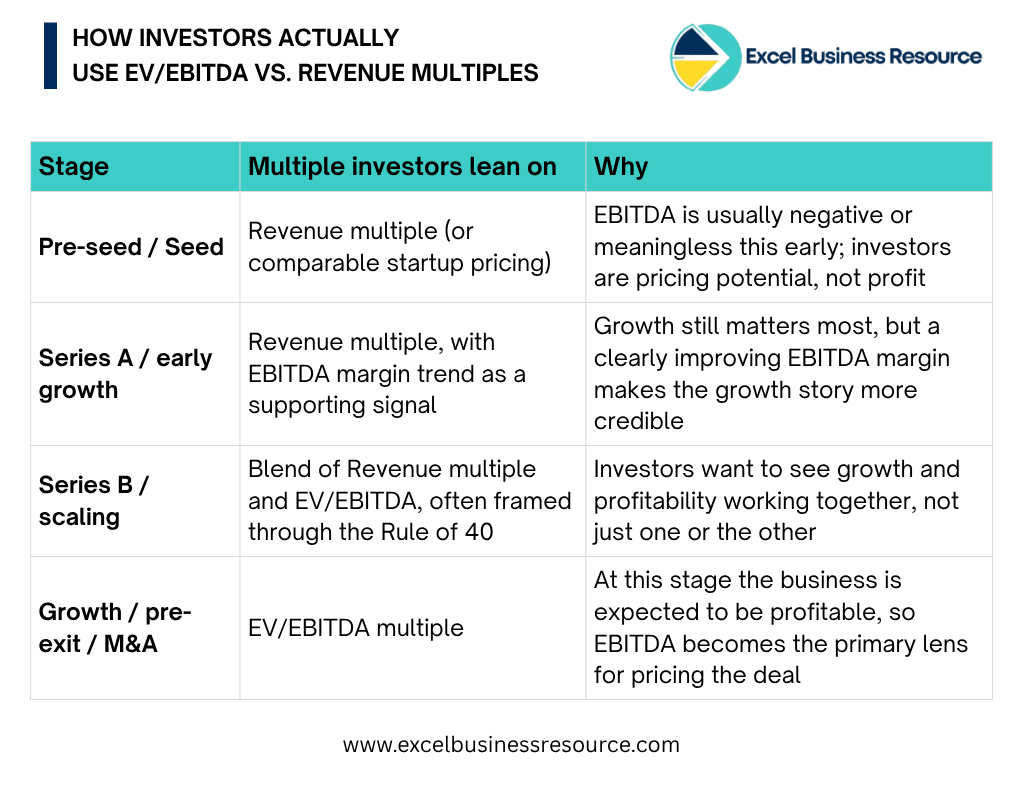

When a startup nears Series B or later, where revenue is more predictable, the EV/EBITDA multiple becomes a real reference point for negotiating valuation, alongside revenue multiples and comparable transactions.

How Investors Actually Use EV/EBITDA vs. Revenue Multiples

Investors don’t pick one valuation multiple and stick with it forever, they shift which multiple matters most as your startup matures. Here’s the general pattern:

The mechanics are simple once you see them laid out: Enterprise Value = EBITDA × Multiple. So if your startup has $2M in EBITDA and your sector’s typical multiple is 8x, an investor’s starting point for enterprise value is roughly $16M. Improve your EBITDA to $3M with the same multiple, and that number jumps to $24M, without raising a single new dollar or adding a single new customer. This is exactly why a stronger EBITDA doesn’t just look good on a slide, it directly multiplies into a higher valuation, because the multiple is doing the heavy lifting on top of whatever EBITDA you bring to the table.

It also explains why a “good” EBITDA matters so much more than founders often assume: investors aren’t just adding your EBITDA to a valuation, they’re multiplying it. A small improvement in EBITDA, or in the quality and durability of that EBITDA, can move enterprise value far more than the same-sized improvement in revenue alone, especially once a company is being priced on profitability rather than growth potential.

It reveals burn quality:

A VC reviewing your model wants to know if your burn is funding genuine growth or masking inefficiency. A model that shows EBITDA improving as a percentage of revenue, even while still negative, tells a much stronger story than one where losses are flat or widening.

It affects how VCs evaluate your financial model:

Investors don’t just glance at your top-line projections, they dig into your assumptions about margins, headcount costs, and operating leverage, all of which roll up into EBITDA. If you want a deeper look at this process, our breakdown of how VCs evaluate the financial model of a startup walks through exactly what investors scrutinize line by line.

It feeds into the broader valuation method:

EBITDA multiples are just one of several approaches investors use alongside DCF, comparable, and venture capital method valuations. If you’re unfamiliar with how these methods interact, our guide to startup valuation methods covers all eight major approaches founders should know before a raise.

What Is a Good EBITDA Margin at Each Funding Stage?

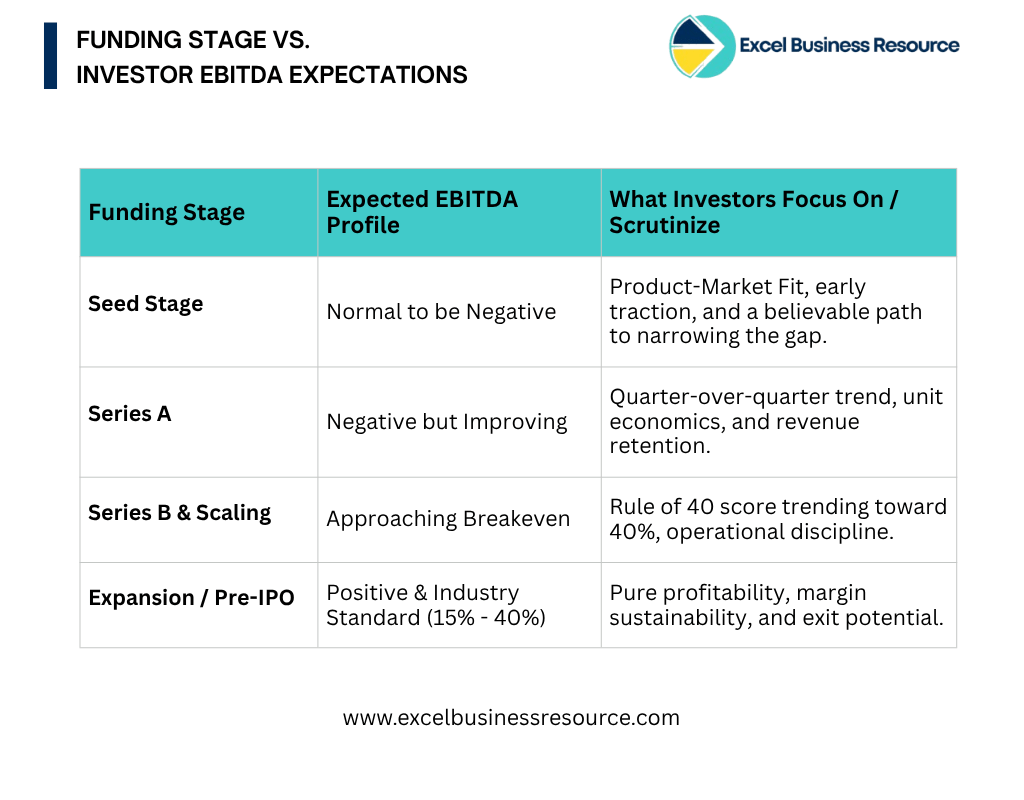

This is one of the most common questions founders ask consultants, and the honest answer is: it changes as you grow. Investors don’t expect the same EBITDA profile from a seed-stage company that they expect from a Series C business. Here’s roughly how that expectation shifts stage by stage:

- Seed stage: A negative EBITDA margin is normal and usually expected. At this point, investors are far more focused on product-market fit, early traction, and the team than on profitability. What they do want to see is a model that shows a believable path toward narrowing that gap, not just a flat or widening loss every month.

- Series A: Investors start paying closer attention to the trend, not just the number. A margin still in negative territory is acceptable if it’s clearly improving quarter over quarter, alongside strengthening revenue growth and retention. This is usually when investors begin asking how your unit economics support a future positive-EBITDA story.

- Series B and scaling stage: As ARR or revenue grows, expectations tighten. Investors increasingly want to see margins approaching breakeven, or a Rule of 40 score (Growth Rate + EBITDA Margin) trending toward 40%. A company growing 60% with a -20% margin can still pass, but the bar gets harder to clear as growth naturally slows with scale.

- Expansion / pre-IPO stage: By this point, EBITDA margin matters in its own right, not just as part of a combined growth-and-profit score. Mature SaaS companies are often expected to show margins in the 20-40% range, while asset-light service businesses commonly sit around 15-25%. Capital-intensive or lower-margin industries naturally run lower, often single digits to mid-teens, and that’s considered healthy within that context.

The pattern across every stage is the same: investors aren’t grading you against a fixed number, they’re grading you against your stage, your industry, and the trajectory of your EBITDA margin over time.

Strategies to Increase Valuation Using EBITDA

Improving EBITDA isn’t about slashing costs across the board, that approach tends to hurt growth and morale. It’s about getting more disciplined about how revenue converts into profit. A handful of strategies tend to move the needle without sacrificing growth:

Improve gross margin first:

Renegotiate supplier or vendor contracts, optimize pricing tiers, and reduce delivery costs. Gross margin improvements flow straight through to EBITDA without touching headcount.

Tighten customer retention:

A relatively small improvement in retention can meaningfully boost profitability over time, since retaining an existing customer is almost always cheaper than acquiring a new one. This is one of the highest-leverage levers available to subscription and recurring-revenue businesses.

Reduce customer acquisition cost (CAC) inefficiency:

If your sales and marketing spend isn’t producing a healthy payback period, it’s dragging EBITDA down without buying you durable growth.

Control fixed overhead as you scale:

Headcount and G&A costs that grow proportionally with revenue erode the operating leverage that should naturally improve your margin as you scale.

Strengthen unit economics before scaling spend:

Chasing top-line growth before your unit economics are solid is one of the fastest ways to scale unprofitability instead of EBITDA.

Model and track EBITDA monthly, not just annually:

You can’t manage what you don’t measure regularly. A model with monthly granularity lets you catch margin erosion early enough to course-correct before it shows up in a board deck.

These aren’t one-time fixes. They’re operating habits that, applied consistently, compound into a meaningfully stronger EBITDA trend, which is precisely what drives a higher valuation multiple at your next raise or exit.

Building EBITDA Correctly Into Your Model

A clean, formula-driven EBITDA line is only as reliable as the financial model underneath it. We’ve worked with 100+ startups across industries on financial modeling, FP&A, and forecasting, and the single most common gap we see is a model where EBITDA exists as a static number rather than a calculated outcome of real assumptions.

If you’re building your model from scratch, our guide to building a startup financial model from scratch walks through the structure needed to get this right from day one. And if your model already exists but you’re not confident in how it’s holding together, our piece on applying effective financial modeling techniques to reduce startup risk is a useful next read.

For founders who’d rather not build this from scratch, our startup financial model templates come pre-built with EBITDA, EBITDA margin, and Rule of 40 calculations already wired into the P&L, across SaaS, e-commerce, manufacturing, and service-based industries. Each template is structured as a driver-based, investment-ready startup financial projection model, so changing one assumption automatically flows through revenue, costs, and EBITDA without you touching a single formula.

Frequently Asked Questions

Not by itself. Most early-stage startups run negative EBITDA while investing in growth. What matters to investors is whether the trend is improving over time and whether the model shows a credible path to positive EBITDA as the company scales.

Less directly, since EBITDA needs revenue and operating costs to be meaningful. Pre-revenue startups are usually valued using methods like the Berkus or Venture Capital method instead. EBITDA becomes relevant once you have consistent revenue and operating history to analyze.

EBITDA is a proxy for operating cash flow, but it isn't identical to it. EBITDA excludes interest, tax, depreciation, and amortization, but it doesn't account for changes in working capital, capital expenditures, or one-time cash outflows. A business can have positive EBITDA and still run short on actual cash.

Many startups present Adjusted EBITDA, which adds back one-off or non-recurring costs like legal fees, restructuring costs, or founder stock-based compensation, to show a cleaner view of ongoing operations. If you do this, be transparent about every adjustment. Investors will ask, and unexplained add-backs damage credibility fast.

Monthly, not just annually. Tracking monthly lets you catch margin erosion early, tie it back to specific drivers like CAC or churn, and walk into investor conversations with a clear, current story instead of stale, year-old numbers.

Yes, frequently. Growth-stage investors weigh EBITDA margin alongside growth rate, which is exactly what the Rule of 40 framework captures. A fast-growing startup with a manageable negative margin can still command a strong valuation if the overall growth-and-efficiency story holds up.

Final Thoughts

EBITDA isn’t just an accounting line item, it’s one of the clearest signals you can give investors about how well you understand and run your business. Getting it right in your model, tracking it consistently, and knowing where you stand against industry benchmarks puts you in a stronger position at every stage of fundraising, from your first pitch deck to a later-stage valuation negotiation.

If you’d rather have an expert build or audit this for you, our team offers custom startup financial planning and FP&A services, along with bookkeeping support, so your numbers are investor-ready before you ever step into a pitch meeting. Get in touch with Excel Business Resource to discuss your financial model, valuation prep, or business plan needs.